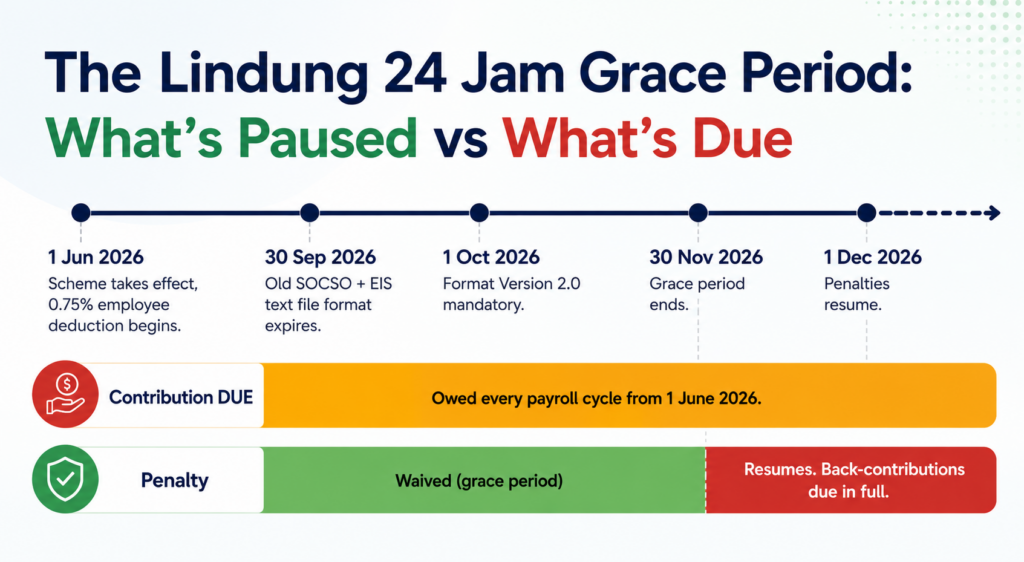

The six-month grace period that came with Lindung 24 Jam is being read across Malaysian HR offices as breathing room. It is not. PERKESO is waiving the penalties for non-compliance during the window. It is not waiving the contribution itself, and the gap between those two things is where the trap sits.

Most companies have not understood the difference, because most companies have not yet read the circular. The headline of the announcement, a six-month grace period for a new statutory scheme, sounds like the kind of soft launch where you can come back to it after the next bonus cycle. The actual mechanics say otherwise.

What Lindung 24 Jam Actually Is

PERKESO’s Non-Employment Injury Scheme, officially the Skim Kemalangan Bukan Bencana Kerja (SKBBK) and branded Lindung 24 Jam, came into force on 1 June 2026 under the Employees’ Social Security (Amendment) Act 2026 (Act A1788). It extends coverage under the Employees’ Social Security Act 1969 (Act 4) to accidents that happen outside the course of employment, within Malaysia, twenty-four hours a day. Workplace accidents stay under the existing Employment Injury Scheme; Lindung 24 Jam sits beside it, not in place of it. More than nine million existing Act 4 contributors, local and foreign, are automatically enrolled.

The financial mechanic is the part that matters for payroll. The contribution is one hundred per cent employee-borne, and the employer’s existing 1.75% SOCSO rate does not change. Employee rates are phased: 0.75% for the first two years, 1.0% for the next three, and 1.25% from year six onwards, capped at the same RM6,000 wage ceiling SOCSO already uses. The Phase 1 contribution works out to a maximum of around RM45 per month per employee.

If you want the wider PERKESO context for how the existing schemes work alongside this, we have written before about how SOCSO operates in Malaysia. Lindung 24 Jam is a new layer over that foundation, not a replacement.

The Grace Period, Read Correctly

The six-month grace period runs from 1 June through the end of November 2026. During that window, PERKESO has said it will not impose penalties for non-compliance with SKBBK specifically. That is the entire scope of the relief.

It does not push the contribution start date. The contribution is owed from 1 June 2026, every payroll cycle, on every eligible employee. Companies that have not configured the deduction by June are not exempt for the months they missed. They are accruing six months of unpaid statutory liability that becomes payable in full, with the penalty cushion removed, the moment the window closes.

Read in that order, the grace period is the opposite of what most HR teams have assumed. It is not a six-month delay. It is a six-month chance to set up properly. After that, the bill arrives whole, and the regulator’s patience does not.

What Has to Happen Before the Window Closes

The work itself is not dramatic, but it is not a single toggle either. Four things have to be in place for every payroll cycle from June 2026 onwards.

The deduction has to exist as a configured line in payroll, calculated at 0.75% on the contributory wage base, capped at RM6,000. The payslip has to show it. Employees will see the new line the first time it appears, and they will ask why their take-home pay has dropped, so HR needs the answer before the first run, not after.

The contribution has to be remitted to PERKESO on the standard monthly schedule, alongside SOCSO and EIS. The SOCSO and EIS contribution text file format has changed to accommodate the new scheme: Format Version 2.0 was published on 13 February 2026, with a new field number eleven for the SKBBK employee share. The old format may still be used until 30 September 2026, after which the new format is mandatory. That is a separate deadline most HR teams have not put on a calendar.

And the records have to be reconcilable. If a SKBBK claim is filed three years from now and the company’s records are unclear about which months were deducted and remitted, the burden of proof sits with the employer, not PERKESO.

Why Your Payroll Setup Matters Here

The companies that will find Lindung 24 Jam straightforward to absorb are the ones whose payroll system already treats each statutory contribution as its own configurable component, not a hard-coded line. Adding a new statutory deduction in that kind of system is configuration. Adding it in a system that bakes the existing statutory items into a fixed structure is a rewrite.

TimeTec Payroll handles SOCSO, EPF, EIS, HRDF and PCB as separate items inside its Statutory Setting, each with its own rate, employee or employer assignment, per-cycle deduction toggle, payslip line, and contribution text-file output. New statutory contributions are added the same way the existing ones are configured, and the per-cycle toggles mean a deduction can be switched on for the correct cycles without disturbing the rest of the run. A scheme like Lindung 24 Jam fits the same architecture rather than forcing a workaround.

The point is not that any single feature solves the problem. The point is that a payroll system built on configurable statutory components absorbs regulatory change as routine work. One built on hard-coded statutory lines absorbs it as a project.

The Date HR Should Have Already Circled

December is not the date that matters. June is. By the time the grace period ends, every monthly payroll run from June through November needs to show SKBBK correctly deducted, correctly remitted, and correctly reflected on the payslip. The companies that did the configuration in May will close the year clean. The companies that left it for after the next holiday or after the audit will close it with backdated contributions due in full and the penalty exemption gone.

The grace period rewards the companies that configured early. It punishes the companies that read it as permission to wait.

The penalty is paused. The contribution is not. A grace period spent doing nothing is not protection. It is a six-month bill that comes due all at once.