Walk into any HR or finance department in Malaysia and you will find a deduction field that nobody questions. Staff loan. Salary advance. Uniform. Training bond recovery. Cash shortage. Damaged stock. Each one sits on the payslip as a clean negative number, processed month after month, signed off without anyone asking the only question that actually matters: was the company allowed to take that money?

Most have never asked it, because the assumption runs the other way: if the system accepted the deduction, it must be legitimate. That assumption is wrong.

A payroll system is not a source of legal authority. It is an instruction follower. Tell it to deduct an amount and it will, whether or not the law permits that amount, because the software has no opinion on Section 24 of the Employment Act 1955. You do not have an illegal-deduction problem because your system is weak. You have one because your system did exactly what it was told.

The clause nobody audits

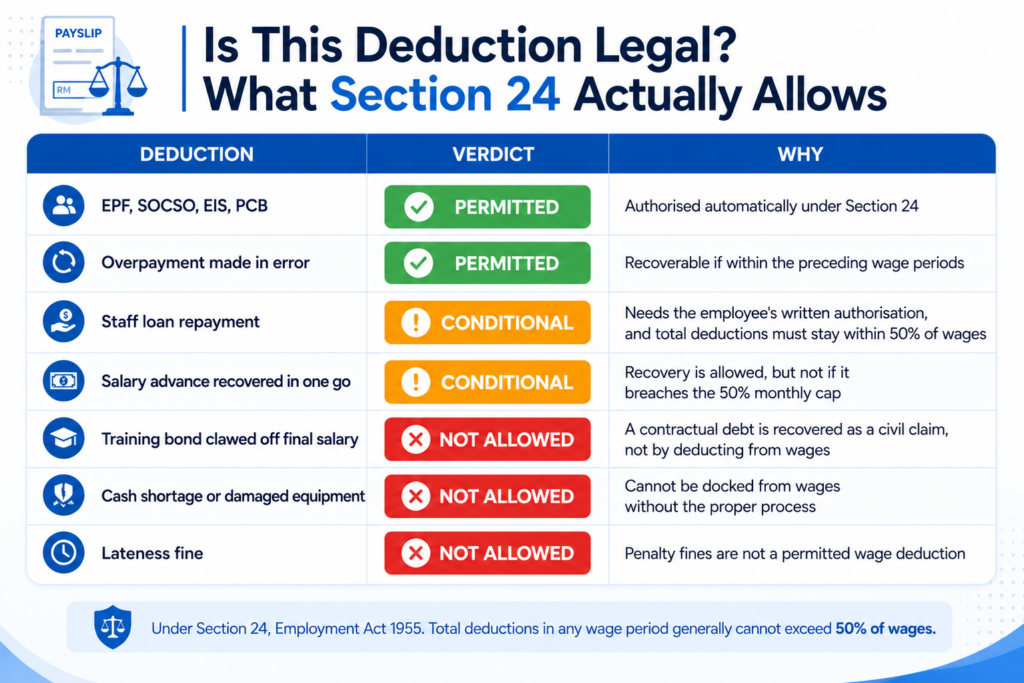

Section 24 sets out what an employer may lawfully subtract from an employee’s wages, and the list is far narrower than most assume. A few deductions are authorised automatically: statutory contributions such as EPF, SOCSO, EIS and PCB; recovery of an overpayment made in error within the preceding wage periods; and indemnity an employee owes for failing to give notice. Advances of wages can also be recovered, though without interest.

Everything else is conditional. Deductions for loan repayments, contributions to a third party, or payments an employee asks the company to make on their behalf all require that employee’s written authorisation. A further set goes beyond even that, demanding the prior permission of the Director General of Labour. And a hard ceiling sits over everything: total deductions in any single wage period generally cannot exceed fifty per cent of that month’s wages.

Read that against how deductions actually get entered into payroll, and the gap becomes obvious.

Where companies quietly cross the line

The training bond is the cleanest example. An employee resigns early, the company wants its training cost back, and so it claws the full amount off the final salary in one stroke. It may well be a valid contractual debt, but such a debt is recovered as a civil claim, not by emptying someone’s last payslip. The deduction takes seconds to process. The authority for it was never there.

Cash shortages and damaged equipment follow the same pattern. A cashier comes up short, a forklift gets dented, a laptop goes missing, and the amount is docked from wages as if the payslip were a settlement mechanism. It is not. Deducting for loss or damage without a proper process is one of the most common breaches in Malaysian payroll, and it is almost always done with full confidence, because the system accepted the number.

Then there is the cap itself. A company advances three months’ salary, then recovers it across two payslips to get it over with. The intention is reasonable. The execution is not: pulling back that much in a single wage period breaches the fifty per cent limit. And lateness penalties dressed up as deductions, fining an employee for clocking in late, fall into a category many systems will happily process and the law generally does not allow at all.

None of these are exotic edge cases. They are the standard contents of the deduction column in most SMEs.

Why the system makes the breach invisible

Here is the dangerous part. An unlawful deduction produces no error. Gross minus deductions equals net, the net figure looks plausible, the bank file balances, and the payslip prints cleanly. The breach is structural, not numerical, which is exactly why a payroll team never catches it: they are checking whether the figures add up, not whether the deduction was permitted.

This is the same blind spot that hides minimum-wage non-compliance. We have written before about how low basic salary dressed up with high allowances quietly breaches the minimum wage, unnoticed until an officer checks the basic-salary line. The deduction column fails the same way: the system shows a number that satisfies everyone except the law.

And the enforcement environment is no longer forgiving. With scrutiny on the wage line tightening and the Department of Labour reaching further into branch operations than it ever has, the deduction column is exactly where an audit lands once it is done with basic salary.

What a payroll system should actually give you

The fix is not a system that refuses unlawful deductions. No software can read a training contract, hold an employee’s written consent, or stand in for the Director General’s approval; those remain documents you keep. What it can do is make every deduction specific and traceable. When an officer asks “show me this RM800 you took,” the answer cannot be a lumped figure on a payslip. It has to be a named deduction, recorded as its own item, with its own amount and its own date.

TimeTec Payroll sets up each deduction as its own salary deduction item, such as Staff Loan, Advance Repayment or Equipment Deduction, rather than a single lumped figure. Each item carries its own amount and can appear as a separate line on the payslip, and the master list of additions and deductions is archived rather than deleted, so historical records survive. Recurring deductions, statutory contributions and the wider salary structure are kept as distinct records, each with its own last-updated trail. The unlawful deduction does not vanish because the system is tidy, but it stops hiding. It becomes a named, dated line you can point to, which is the difference between a deduction you can stand behind and one you discover during an audit.

The deduction that looks routine until someone asks

Every deduction in the column looks justified on its own. The staff loan the employee agreed to repay. The shortfall from a till that did not balance. The training the company paid for and wants back. Each one has a reason, and the reason usually sounds fair.

Fairness is not the test. The test is whether Section 24 permitted the deduction, whether the employee authorised it in writing, whether it needed the Director General’s approval, and whether it stayed within the fifty per cent cap. A deduction can be entirely reasonable and entirely unlawful at the same time.

A clean payslip and a lawful one are not the same thing. The payslip records what you deducted; Section 24 decides whether you were allowed to. A payroll system that cannot answer the second question is not protecting you. It is documenting the breach in your own handwriting.